The Financial Mirror 05/02/2015

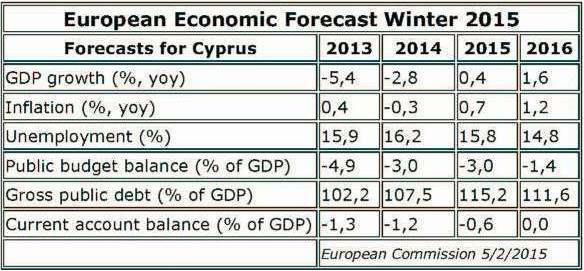

The Cyprus economy is showing signs of stabilisation, with mild growth rates of 0.4% this year and 1.6% in the next, but the improvement in economic sentiment indicators has come to a halt, according to the European Commission’s Economic Forecast for Winter 2015.

While lower oil prices are expected to support growth, external demand will suffer from headwinds from the Russian economy and fiscal consolidation is expected to continue, the forecast said.

The forecast figures for Cyprus will be updated after the sixth review of Cyprus’ Economic Adjustment Programme has taken place, which has currently been suspended due to a delay in the introduction of a framework for foreclosures and insolvencies, an obligation as part of the EUR 10 bln bailout plan with the Troika of international lenders.

GDP BOTTOMING OUT

Economic activity declined by 1.7% y-o-y in the third quarter of 2014, a slight improvement relative to the second quarter, driven by developments in private consumption and investment, including a one-off large purchase of transport equipment, which also boosted imports. Excluding this transaction, the growth momentum in both real imports and real investment remained subdued, the EC forecast said.

Real exports weakened in the third quarter, down 4.5% y-o-y, which associated with the temporary pick-up in imports has worsened the current account.

Unemployment has been flat hovering around 16%, with continued, albeit slower, contraction in employment offset by a further fall in labour force.

Against the background of low capacity utilisation and continued wage adjustment, inflationary pressures remain weak. HICP inflation in 2014 has been supported by prices of goods consumed by tourists, while prices of goods consumed by locals have continued to fall and energy prices fell strongly as well in end-2014.

ECONOMIC SENTIMENT FLAT

Economic sentiment remained broadly unchanged in the second half of 2014, putting on hold the improvement observed since April 2013. While consumer confidence continued to improve, business sentiment in most sectors weakened with the exception of service sector confidence which improved somewhat.

Although retail trade indicators suggest an improving growth momentum in the short term, this is offset by weakness in short-term indicators for credit and tourist arrivals, in particular Russian tourists, reflecting the negative economic developments in Russia.

TIMID RECOVERY IN 2015-2016

In 2015 and 2016, growth is forecast to resume only gradually as private domestic demand slowly picks up supported by lower energy prices, the EC forecast said.

GDP growth is expected to reach 0.4% this year and 1.6% in 2016, after a contraction of -5.4% in 2013 and -2.8% last year.

This should be accompanied by gradual deleveraging of both households and corporates and a reduction of the non-performing loans (NPL) ratio (now at close to 50%) down to more sustainable levels. The moderate pick-up in domestic demand is expected to be reflected into improved labour market conditions, with unemployment starting to ease gradually. HICP inflation is also expected to remain low, weighed down by recent declines in oil prices.

SOME DOWNSIDE RISKS

Risks to the recovery are tilted to the downside, the EC winter forecast said, explaining that on the domestic front, a failure to reduce the high NPL ratios could lead to a more prolonged period of tight credit supply conditions, stalling the recovery of investment.

On the external side, negative economic developments in Russia are likely to weigh on export growth in 2015, given the sizeable trade links between Russia and Cyprus.

This negative effect is likely to dominate the positive impact from lower oil price, leading to downside risk to the GDP growth projection for 2015. Risks to the HICP inflation also remain on the downside, largely due to lower energy prices.

STRONG FISCAL ADJUSTMENT

In 2014, the general government headline and primary balance are projected to improve sharply by about 2% of GDP, on the back of further consolidation measures.

Revenue is expected to increase compared to 2013, driven by consolidation measures, high dividends from the Central Bank of Cyprus, and improved tax collection.

Together, these factors should more than offset the negative impact of slowing economic activity on income and wealth taxes proceeds. Total expenditure is expected to remain on a decreasing path, despite an adverse impact due to called government guarantees. This largely reflects tight expenditure control, measures under Cyprus’ adjustment programme to reduce the public sector wage bill, and a moderation of early retirements in the public sector, which reduced the cost of lump-sum pension payments.

The general government deficit is expected to stabilise in 2015 and to decrease significantly in 2016, as better economic conditions should have a positive impact on revenues, the EC forecast said.

Further consolidation efforts needed under the adjustment programme with the Troika should support these developments. The projections include dividend income from the Central Bank of Cyprus expected to amount to 0.6% of GDP in both 2015 and 2016, to be distributed in line with the CBC's duties under the various EU treaties and the ESCB and ECB Statute.

Cyprus' debt-to-GDP ratio is expected to peak in 2015 and to decline afterwards, supported by the economic recovery and the fiscal performance. Compared to the previous forecast, the debt-to-GDP ratio is positively affected by the upward revision of nominal GDP by about 10% due to the transition to ESA2010 and other statistical benchmark revisions.